Using an LLC in Your Estate Plan

Learn how limited liability companies can protect assets, ease transfers to heirs, and complement trusts and wills in modern estate planning.

Estate planning is no longer limited to wills and trusts. Today, many families and business owners are turning to the limited liability company (LLC) as a flexible tool for protecting assets, managing investments, and planning for the transfer of wealth to the next generation.

This guide explains how LLCs work in an estate planning context, why they can be useful, and what you should consider before making one part of your long‑term plan.

What Is an LLC and Why Does It Matter for Your Estate?

An LLC is a business structure that combines the liability shield of a corporation with the flexible taxation and management of a partnership. While LLCs are often associated with operating businesses, they can also hold investment accounts, rental properties, or other assets as part of an estate plan.

Key characteristics that make LLCs attractive for estate planning include:

- Limited liability: Members are generally not personally responsible for the debts and liabilities of the LLC, helping shield personal wealth from claims against the entity.

- Pass‑through taxation: By default, the LLC itself is not taxed; income and losses flow through to the members and are reported on their individual returns.

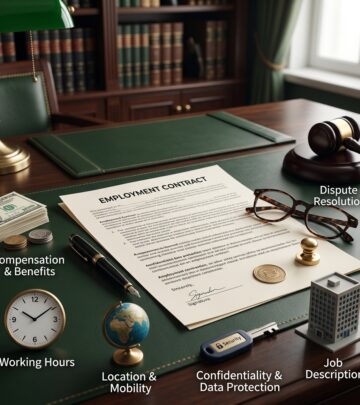

- Contractual flexibility: The operating agreement can be customized to manage control, voting rights, distributions, and restrictions on transfers of ownership.

These features allow an LLC to serve as both a management wrapper around family assets and a vehicle for gradually shifting ownership to heirs.

Common Ways LLCs Are Used in Estate Planning

LLCs can play several roles in a comprehensive estate plan. The strategy depends on the type of assets you own, your family dynamics, and your long‑term goals.

LLCs for Real Estate and Rental Properties

One of the most frequent uses of LLCs in estate planning is to hold residential or commercial real estate. Placing property in an LLC can:

- Provide a liability buffer if someone is injured on the property or if a tenant sues.

- Keep ownership records in the name of the LLC instead of your personal name, improving privacy.

- Allow you to transfer membership interests to children or other heirs instead of retitling the real estate each time ownership changes.

Bad Credit Personal Loans: A Practical Legal Guide >

Financial institutions and wealth managers note that holding real estate in an LLC can also streamline management of multiple properties and make succession planning more predictable.

Family Investment LLCs

Families sometimes establish an LLC to pool investment accounts, cash reserves, and other marketable assets into one entity. This approach can:

- Centralize decision‑making under one or more managers.

- Provide a structure for educating younger family members about investing.

- Support gradual transfers of economic interests while maintaining senior generation control through voting or management rights.

Such LLCs are often referred to as family LLCs or family holding companies. They allow parents or grandparents to gift or sell non‑voting interests to descendants while retaining management authority in their own hands or in a trusted group of managers.

LLCs Paired with Trusts and Wills

LLCs typically do not replace core estate planning documents. Instead, they complement wills and trusts by serving as the legal owner of specific assets.

In a coordinated plan, you might:

- Place real estate or investments into an LLC.

- Designate your revocable living trust or children as the beneficiaries of your LLC interests.

- Use your will to handle personal property and any remaining assets not already titled to the LLC or trust.

When you die, the ownership interests in the LLC can pass under the terms of your trust or will, often avoiding the need to retitle each underlying asset individually.

Advantages of Using an LLC in Your Estate Plan

The benefits of incorporating an LLC into estate planning touch on asset protection, tax considerations, administration, and family governance.

1. Asset Protection and Liability Shield

LLCs are widely used because they separate business or investment risks from the owners’ personal assets. If a claim arises from an asset owned by the LLC—such as a tenant injury at a rental property—the creditor typically can pursue only the LLC’s assets, not your personal home, car, or savings, assuming proper separation and formalities are maintained.

Estate planners often view this liability shield as a way to protect the family balance sheet from litigation and unexpected claims tied to specific assets.

2. Privacy and Discretion

Real estate records and certain financial filings are public. When assets are held directly in your name, anyone researching those records may identify you as the owner. An LLC can provide a layer of privacy by listing the entity as the owner in property records, which may make it harder for casual observers to connect specific assets to you personally.

While transparency rules vary by state, using an LLC can be part of a broader strategy to reduce public visibility of your holdings, especially when combined with trusts and other planning tools.

3. Flexible Tax Treatment

From a tax perspective, LLCs offer considerable flexibility. By default, an LLC with a single owner is treated as a disregarded entity, and an LLC with multiple owners is treated as a partnership for federal income tax purposes. In either case, income flows through to the members and is typically taxed once at the individual level.

Members can sometimes elect to have the LLC taxed as a corporation, including S corporation or C corporation status, depending on their needs. This ability to choose taxation can be helpful when coordinating an estate plan with other tax strategies, especially for families with complex income profiles.

4. Control Over Transfers to Heirs

The LLC operating agreement can include detailed rules about who may become a member, how interests may be transferred, and what happens when a member dies or becomes incapacitated. This allows you to:

- Restrict transfers to non‑family members.

- Require consent before interests are sold or gifted.

- Define buy‑out rights, valuation methods, and dispute resolution procedures.

By formalizing these rules, you can reduce the risk of conflict among heirs and preserve the continuity of asset management after your death.

5. Streamlined Management of Complex Assets

Holding multiple properties or investment accounts can become administratively burdensome. An LLC acts as a single organizational umbrella under which various assets are grouped. This consolidated structure can:

- Make recordkeeping, accounting, and reporting more efficient.

- Simplify succession by transferring interests in one entity rather than multiple separate titles.

- Provide clarity about who has authority to sign contracts, leases, or other documents.

In practice, an LLC can serve as the operating hub for a family’s investment and real estate activities, which often makes ongoing management easier for the next generation.

Potential Drawbacks and Limitations

Despite their advantages, LLCs are not an automatic solution for every estate planning situation. You should be aware of several limitations and costs.

Administrative and Compliance Requirements

Forming and maintaining an LLC involves state filings, fees, and ongoing obligations such as annual reports or franchise taxes. While generally less complex than a corporation, an LLC still requires:

- Proper formation documents filed with the state.

- A well‑drafted operating agreement.

- Separate bank accounts and bookkeeping to maintain the liability shield.

For smaller estates or simple asset holdings, the added structure may not be worth the effort or expense.

State‑Specific Rules and Tax Treatment

LLC laws and tax rules differ from state to state. Factors such as formation fees, reporting requirements, privacy provisions, and state income or franchise taxes can influence whether an LLC is appropriate.

Because real estate is governed by the state where it is located, you may need to form or register an LLC in that jurisdiction for property‑holding purposes. Professional advice is important to ensure the structure aligns with state law and does not create unintended tax obligations.

Not a Substitute for Core Estate Documents

LLCs manage ownership and liability, but they do not replace a will or trust. Without proper estate planning documents to direct what happens to your LLC interests on death, your ownership may still pass through probate, which can be public and time‑consuming.

For most people, an LLC is best viewed as a component of a broader plan rather than a standalone solution.

LLC vs. Other Estate Planning Tools

To decide whether an LLC fits your situation, it helps to compare it with other common estate planning structures.

| Feature | LLC | Revocable Trust | Owning Assets Individually |

|---|---|---|---|

| Liability protection | Yes, for business/asset‑related claims if respected formalities are followed. | No direct liability shield; focuses on asset transfer and management. | None; personal assets are exposed to claims and lawsuits. |

| Privacy of ownership | Moderate; assets can be titled to the LLC rather than individuals. | High; trust ownership may avoid public probate in many situations. | Low; titles and probate records often list personal names. |

| Tax treatment | Flexible; typically pass‑through, with options to elect corporate status. | Generally tax neutral during life; income taxed to the grantor. | Standard individual taxation based on asset type. |

| Transfer at death | Membership interests pass via will or trust; may still involve probate without planning. | Assets can pass outside probate according to trust terms. | Probate often required to retitle assets. |

| Management during incapacity | Managers can continue operating the LLC if authorized in the operating agreement. | Successor trustee can seamlessly manage assets. | Requires powers of attorney or court‑appointed guardian. |

In many cases, families use both trusts and LLCs together: the LLC holds the assets and the trust holds the LLC interests, providing liability protection plus probate avoidance and clear succession rules.

When Might an LLC Make Sense for Your Estate Plan?

No single structure is right for everyone. However, certain scenarios commonly benefit from an LLC‑based approach:

- Multiple rental properties or investment real estate: An LLC can help segment liability and simplify management.

- Family‑owned business or closely held investments: An LLC facilitates shared ownership and succession planning among relatives.

- Desire for privacy: Titling assets to an entity can reduce direct public association with your name.

- Gifting strategy: You want to gradually transfer economic interests while maintaining centralized control.

On the other hand, families with few assets, no business or rental activity, and simple inheritance goals may find that a will and basic trust cover their needs without the added complexity of an LLC.

Practical Steps to Integrate an LLC into Your Estate Plan

If you decide to explore using an LLC as part of your estate plan, consider the following practical steps:

1. Clarify Your Objectives

Before forming an entity, identify what you are trying to accomplish. Common objectives include:

- Protecting personal assets from business or property‑related liabilities.

- Creating a framework for shared family investments.

- Structuring gradual transfers of wealth to younger generations.

- Improving the privacy of your holdings.

Clear goals will inform choices about the type of LLC, its ownership structure, and how it interacts with your other planning documents.

2. Consult Legal and Tax Professionals

Because LLCs are governed by state law and have tax consequences, it is important to consult an attorney and a qualified tax advisor when integrating them into an estate plan. They can help you:

- Select the appropriate state for formation and understand any registration requirements.

- Draft an operating agreement tailored to your family and asset mix.

- Coordinate the LLC structure with existing wills, trusts, and powers of attorney.

- Evaluate potential gift and estate tax implications of transferring interests.

3. Formalize the Operating Agreement

The operating agreement is the backbone of an estate‑focused LLC. It should address:

- Who may be members and how new members are admitted.

- Management roles, voting rights, and decision‑making procedures.

- Restrictions on transfers of interests, including what happens at death or divorce.

- Distribution policies and how cash flow is shared among members.

A carefully drafted agreement can prevent disputes and provide predictability when assets pass to heirs.

4. Coordinate Ownership and Beneficiary Designations

Once formed, the LLC must actually own the relevant assets. This involves retitling real estate, investment accounts, or other property to the LLC’s name where appropriate and allowed. At the same time, you can:

- Update your will or trust to describe how your LLC interests should be distributed.

- Review beneficiary designations on life insurance or retirement accounts so they align with your overall plan.

Proper coordination reduces the risk of assets being left out of the entity or passing in ways that conflict with your intentions.

SEO‑Friendly FAQs About LLCs and Estate Planning

Is an LLC better than a trust for estate planning?

Neither structure is universally better. An LLC primarily offers liability protection and organizational benefits for assets such as real estate and family businesses. A revocable trust focuses on probate avoidance, privacy, and management during incapacity. Many comprehensive plans use both—LLCs to hold certain assets and trusts to hold the LLC interests.

Can an LLC help avoid probate?

Standing alone, an LLC does not necessarily avoid probate. However, if your LLC interests are titled to a trust or are subject to well‑crafted transfer provisions, probate of those interests may be reduced or avoided in some jurisdictions. The underlying assets do not need to be retitled individually, which can streamline administration.

Does using an LLC reduce estate or gift taxes?

LLCs do not automatically reduce estate or gift taxes, but they can support strategies that involve gradual transfers of interests and clear valuation methods. For example, transferring minority or non‑voting interests may involve different valuation considerations. Professional tax advice is essential when using LLCs in any transfer‑tax planning.

Is an LLC appropriate for a small estate?

For modest estates with few assets and no rental or business activities, the compliance costs and complexity of an LLC may outweigh the benefits. A simple will, and in some cases a basic trust, might be sufficient. An LLC becomes more compelling when there are liability‑prone assets or multiple family owners to coordinate.

How do I choose the state for forming my estate planning LLC?

The appropriate state depends on where your assets are located and where you live. Real estate usually dictates its own jurisdiction, so an LLC holding property is commonly formed or registered in the state where that property sits. When privacy, tax, or regulatory considerations arise, an attorney can help compare different states’ rules.

References

- Proteja los activos personales a través de una LLC inmobiliaria — PNC Bank. 2023-05-10. https://www.pnc.com/insights/es/wealth-management/living-well/protect-personal-assets-through-a-real-estate-LLC.html

- ¿Cuáles son las ventajas de una LLC y por qué debería formar una? — Law 4 Small Business. 2022-08-01. https://www.l4sb.com/blog/what-are-the-advantages-of-the-llc-form-of-organization/

- 10 Beneficios Fiscales de Tener una LLC en Estados Unidos — Defentux. 2023-03-15. https://defentux.com/10-beneficios-fiscales-de-tener-una-llc-en-estados-unidos/

- Proteja los activos personales a través de una LLC inmobiliaria — PNC Bank. 2023-05-10. https://www.pnc.com/insights/wealth-management/living-well/protect-personal-assets-through-a-real-estate-LLC.html

- Key Benefits of Structuring Your Business as an LLC — J.A. Gonzalez Law. 2022-11-20. https://es.jagonzalezlaw.com/blog/business-formation/key-benefits-of-structuring-your-business-as-an-llc/

Similar Articles

Read full bio of medha deb