Understanding Bank Loan Disputes

A practical guide to the most common conflicts that arise in bank lending relationships.

Disputes involving bank loans can arise long before a borrower stops making payments and can continue well after default. These conflicts often turn on the meaning of a promissory note, the timing of payments, the treatment of collateral, or whether the lender followed required procedures when enforcing the loan. In many cases, the issue is not simply that money is owed, but that one side believes the other side acted unfairly, incorrectly, or in violation of the loan documents.

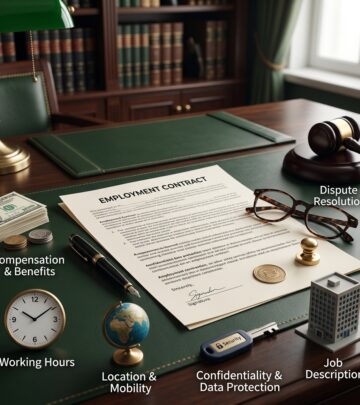

When a bank loan disagreement escalates, the parties may need to rely on contract law, consumer protection rules, foreclosure law, or general civil litigation. Loan disputes are usually document-heavy, and the most important evidence often includes the note, the loan agreement, payment records, notices, emails, and any correspondence about default or restructuring. Because the legal consequences can be significant, both borrowers and lenders benefit from understanding the points where these disagreements typically begin.

What usually triggers a bank loan dispute

Most bank loan disputes begin with a disagreement about performance under the loan documents. A borrower may believe payments were made on time, while the bank treats the account as delinquent. In other cases, the borrower may object to added fees, changes in interest calculation, an acceleration notice, or the lender’s decision to call the balance due earlier than expected. Loan litigation generally centers on these written instruments and requires the parties to prove their positions with admissible evidence.

- Missed or disputed payments

- Interest calculation errors

- Acceleration of the full balance

- Problems with collateral or security interests

- Claims that the lender acted improperly during enforcement

Sometimes the disagreement starts with a narrow accounting issue but expands into broader allegations of misconduct. If the parties cannot resolve the matter informally, the conflict may become a civil case in which the court evaluates both the loan terms and the conduct of each side.

Common types of bank loans and why the category matters

Bank loans are not all the same. Personal loans, home loans, auto loans, student loans, and small business loans each serve different purposes and are governed by different documents and practical expectations. A home loan often raises foreclosure questions, while a business loan may involve collateral, guaranties, or allegations that the lender interfered with business operations. Understanding the type of loan matters because it affects the remedies available and the procedures the lender must follow.

| Loan type | Typical purpose | Common dispute issues |

|---|---|---|

| Personal loan | Debt consolidation or large purchases | Payment timing, fees, interest disputes |

| Mortgage | Financing a home | Foreclosure, notice defects, acceleration |

| Auto loan | Vehicle purchase | Repossession, account balances, insurance issues |

| Student loan | Education expenses | Repayment terms, servicing issues, documentation |

| Small business loan | Startup or expansion capital | Collateral, guaranties, lender interference |

The same general dispute can look very different depending on the loan category. For example, a missed payment on a mortgage may lead to foreclosure proceedings, while a similar issue in a business loan may lead to a demand letter, acceleration, or a lawsuit over the loan agreement.

Borrower concerns that often lead to litigation

Borrowers often bring claims when they believe the bank overstepped the terms of the agreement. A lender may be accused of charging fees not authorized by the note, misapplying payments, or declaring default too quickly. Some disputes focus on the lender’s treatment of collateral, especially when the lender attempts to seize or sell property before complying with the required procedures. Courts generally require lenders to follow the contract and any applicable procedural protections carefully, particularly in foreclosure settings.

Another common borrower concern is the lender’s use of contract language in a way that feels technically correct but commercially unreasonable. In some situations, courts have recognized that lenders can face liability if they foreclose or accelerate a loan based on a mere technical default, especially where the lender’s conduct appears inconsistent with good faith or the purpose of the loan relationship.

- Unauthorized fees or charges

- Incorrect payment posting

- Early acceleration of the debt

- Improper foreclosure or repossession steps

- Alleged breach of the duty of good faith and fair dealing

Lender concerns and enforcement rights

Banks also face real risks when borrowers stop paying or violate loan covenants. A lender may decide to issue default notices, demand immediate payment, seize collateral, or file suit to recover the balance. These responses are often permitted by the contract, but only if the lender acts within the bounds of the agreement and applicable law. Loan litigation is a formal process, and the lender must prove the debt, the default, and the basis for the remedy sought.

In business lending, enforcement can become especially complex when collateral, personal guarantees, and cross-default provisions are involved. The lender may believe it is simply protecting its security interest, while the borrower may argue that the lender acted too aggressively or used the threat of default to gain leverage unrelated to repayment. Where lenders fail to comply with required foreclosure procedures, they may create exposure beyond the unpaid balance itself.

When lender conduct crosses the line

Not every hard collection action creates liability, but lender conduct can become actionable when it goes beyond ordinary enforcement. Some legal claims arise when the bank makes false statements, hides material information, interferes with a borrower’s business, or uses its position to control a company’s operations. In certain cases, lenders that move from creditor to de facto operator can face claims involving breach of duty, confidentiality concerns, or self-interested conduct.

Separate cases also recognize traditional causes of action such as breach of contract, fraud, tortious interference, and bad-faith enforcement. The exact claim depends on the facts, the wording of the loan documents, and the law in the relevant state.

- Breach of contract

- Fraud or misrepresentation

- Tortious interference with business relationships

- Breach of the covenant of good faith and fair dealing

- Wrongful foreclosure or improper collateral enforcement

How loan disputes are usually resolved

Many loan disputes are settled before trial through negotiation, forbearance agreements, repayment plans, or loan modifications. If settlement fails, either side may file a civil complaint. Once litigation begins, the court process requires each party to support its claims with documents and testimony rather than informal complaints or assumptions.

Borrowers may try to defend against the lender’s claims by showing that payments were timely, that the bank made accounting errors, or that the bank failed to provide required notices. Lenders may counter with records showing default, contractual authorization for acceleration, or compliance with enforcement procedures. In many disputes, the outcome depends on whether the bank can prove that it acted according to the written agreement and the law governing the transaction.

Practical steps for borrowers who think a bank is wrong

Borrowers who suspect a problem should act quickly and preserve records. The strongest disputes are usually built from account statements, letters, emails, screenshots, and copies of the loan documents. A borrower should compare the bank’s numbers to personal records and identify the exact transaction, fee, or notice being challenged.

- Gather the loan agreement and all amendments

- Save payment confirmations and bank statements

- Keep copies of every notice or demand letter

- Write down dates, names, and the substance of phone calls

- Request clarification before the dispute grows

If the dispute involves incorrect account information or servicing errors, a borrower may also need to submit a formal written complaint to the company or a consumer regulator. The Consumer Financial Protection Bureau advises consumers to be clear, include key dates and amounts, and attach supporting documents when submitting a complaint. For credit reporting issues tied to a loan, consumers are generally told to dispute the error with the credit bureau and include written explanations and supporting records.

Practical steps for banks and loan servicers

Banks reduce their litigation risk by keeping thorough records and following their own procedures consistently. Clear notices, accurate payment histories, and careful use of default and acceleration clauses are essential. When a borrower claims an error, the lender should review the account promptly and respond in writing where appropriate. A lender that cannot document its own position may have difficulty defending an enforcement action later.

For commercial loans, lenders should also avoid conduct that could be interpreted as controlling day-to-day business decisions unless the agreement clearly permits that level of involvement. Once a lender becomes too involved in management, the dispute can shift from a simple debt collection matter to a broader lender-liability case.

Evidence that matters most in a loan dispute

Because bank loan disputes are heavily document-based, the strongest cases often come down to a small set of records. Courts and regulators are more persuaded by paper trails than by general accusations. The key question is usually not whether the parties disagree, but whether the party making the claim can prove it.

| Evidence | Why it matters |

|---|---|

| Promissory note and loan agreement | Shows the contractual terms and remedies |

| Payment history | Reveals whether default actually occurred |

| Default or acceleration notices | Shows whether required notice was sent |

| Collateral records | Important in foreclosure and repossession disputes |

| Emails and letters | Help prove what each side knew and said |

Frequently asked questions

Can a bank sue if I miss one payment? Yes, if the loan documents allow default or acceleration after a missed payment, but the lender must still follow the contract and any required notice procedures.

What if the bank charged the wrong amount? A borrower may dispute the accounting, ask for corrections, and raise the issue as a defense or counterclaim if the matter becomes a lawsuit.

Can a lender be liable for aggressive collection? Yes. Depending on the facts, lenders may face claims for breach of contract, fraud, interference, or improper foreclosure-related conduct.

What should I save if I expect a dispute? Keep the loan contract, statements, notices, and every piece of written communication with the bank. Those documents usually become central evidence in any later case.

Why these disputes often turn on procedure

Bank loan disputes are frequently won or lost on procedure rather than sympathy. A borrower may have a strong sense that the bank acted unfairly, but a court usually needs proof that the bank violated the note, failed to send a required notice, misstated the balance, or breached a legal duty. Likewise, a lender that wants to foreclose, repossess, or sue on a note must show that it followed the required steps and can document the debt accurately.

That is why both sides should approach these disagreements as evidence-driven matters. The faster a party identifies the exact contractual issue, the better the chance of resolving the dispute before it becomes expensive litigation.

References

- How to Use the Law to Fight Bank Abuse — JC White Law. 2025-04-28. https://jcwhitelaw.com/2025/04/28/how-to-use-the-law-to-fight-bank-abuse/

- Resolving Disputes Over Loan Defaults and Repayment Obligations — Daeryun Law. 2025. https://www.daeryunlaw.com/us/practices/detail/loan-litigation

- Banking Disputes and Lender Liability — Drew Cooper & Anding. 2025. https://dca-lawyers.com/practices/business-and-corporate/banking-disputes-and-lender-liability/

- Disputing Errors on Your Credit Reports — Federal Trade Commission. 2024. https://consumer.ftc.gov/articles/disputing-errors-your-credit-reports-0

- How do I dispute an error on my credit report? — Consumer Financial Protection Bureau. 2024. https://www.consumerfinance.gov/ask-cfpb/how-do-i-dispute-an-error-on-my-credit-report-en-314/

- Disputes Over Bank Loans — LegalMatch. n.d. https://www.legalmatch.com/law-library/article/disputes-over-bank-loans.html

- Submit a complaint — Consumer Financial Protection Bureau. 2024. https://www.consumerfinance.gov/complaint/

Similar Articles

Read full bio of Sneha Tete