ACA Employee Benefits: Employer Rules Explained

A practical guide to employer health coverage duties, eligibility, and ACA compliance.

The Affordable Care Act changed the way many employers handle health coverage, especially for full-time workers and their dependents. For businesses that meet the law’s size threshold, the central issue is not whether they may offer coverage, but whether the coverage is offered on terms that satisfy federal standards.

This article explains the main ACA employee benefit rules in plain language. It covers which employers are affected, how full-time status is measured, what makes coverage affordable and meaningful, and which reporting duties can create compliance risk. The goal is to give employers and workers a clear framework for understanding workplace health benefits under the ACA.

Why the ACA Matters for Employer Benefits

The ACA is more than a health insurance law for individuals. It also created obligations for certain employers that sponsor group health plans. Those rules were designed to expand access to coverage, reduce gaps in insurance, and make employer-sponsored plans more consistent across workplaces.

For many employers, the ACA operates as a “pay or play” system. In simple terms, a large employer must either offer qualifying health coverage to enough full-time employees or face the possibility of a penalty if workers turn to a marketplace plan and receive premium assistance. That structure makes benefit administration a legal compliance issue, not just an HR decision.

Which Employers Are Covered

The ACA’s employer mandate applies primarily to large employers, often called applicable large employers, or ALEs. These are generally employers with at least 50 full-time employees, counting full-time equivalent workers as part of the calculation. Smaller employers are usually not subject to the same mandate, though they may still choose to offer coverage and may have access to tax-related incentives.

Because the threshold depends on workforce size, employers need a reliable method for tracking hours worked. The number of employees on payroll is not always the same as the number of employees counted under the ACA. Part-time and variable-hour staff can affect whether a business crosses the line into ALE status.

| Employer Size | General ACA Rule |

|---|---|

| Under 50 full-time employees | Usually not subject to the employer coverage mandate |

| 50 or more full-time employees | May be required to offer qualifying coverage to eligible workers and dependents |

How Full-Time Status Is Measured

Under ACA rules, a full-time employee is generally one who averages at least 30 hours of service per week, or 130 hours per month. Employers may use look-back measurement methods to evaluate workers whose schedules vary, including seasonal, temporary, and on-call employees.

This matters because benefit eligibility is not always based on a single week’s schedule. Instead, employers may review hours over a defined measurement period, then assign coverage during a stability period if the employee meets the full-time threshold. The result is that employees can remain eligible for coverage even if their hours later drop, so long as the stability period is still running and the person remains employed.

- Full-time standard: 30 hours per week or 130 hours per month.

- Measurement periods: Used to evaluate workers with changing schedules.

- Stability periods: Coverage can continue for a set time after eligibility is established.

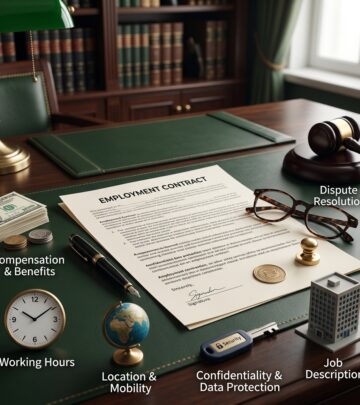

What Coverage Must Include

Offering a health plan is only part of the ACA requirement. The plan must also satisfy federal benefit standards. Two of the most important are minimum essential coverage and minimum value.

Minimum essential coverage refers to coverage that meets the ACA’s basic insurance requirement. Minimum value means the plan is designed to pay at least 60% of the total allowed cost of covered services for a standard population. That does not mean every employee gets 60% of his or her medical bills paid in every case; rather, it is an actuarial benchmark used to measure the plan’s generosity overall.

Employer plans must also remain attentive to broader ACA benefit expectations, such as coverage for preventive care and other health services commonly associated with comprehensive medical insurance. In practice, the law pressures employers to offer coverage that is not merely nominal, but genuinely useful.

Affordability: The Price Test Employers Must Watch

ACA compliance also depends on affordability. A plan may fail the law even if it offers solid benefits, because the employee share of the premium is too expensive. The affordability test focuses on whether the employee’s required contribution is below a statutory percentage of household income, though employers often rely on safe harbors because they usually do not know each worker’s household income.

This rule matters most for lower-wage employees. If the worker’s contribution is too high, the employer may still be treated as having failed to offer affordable coverage. That can trigger penalty exposure if the employee receives a subsidy through the marketplace.

- Affordable coverage: Employee premium contribution must stay under the federal percentage limit.

- Practical challenge: Employers often use proxy methods because household income is not always known.

- Risk point: Expensive employee-only coverage can cause problems even when a plan exists.

Dependents and the Age 26 Rule

The ACA also reshaped dependent coverage. Employers that offer dependent health benefits generally must make coverage available to an employee’s children until age 26. This rule is one of the law’s best-known protections and has become a standard feature of many employer plans.

In practical terms, the dependent coverage rule means employers should check plan documents carefully. A plan that excludes young adult children, or that ends coverage too early, may not satisfy ACA expectations. Employers should also coordinate enrollment procedures so that dependent eligibility is clear and easy to administer.

Grandfathered Plans and Exceptions

Not every older health plan is subject to the same ACA changes. Some plans that were already in existence when the law was enacted may be treated as grandfathered if they have not been significantly altered. These plans can be exempt from certain ACA requirements, but the exemption is limited and may be lost if the employer makes major changes.

Grandfathered status can be useful, but it should not be assumed. Employers that believe they have such a plan should review plan amendments, benefit changes, contribution shifts, and coverage revisions to see whether the status still applies.

Employer Reporting Duties

Coverage decisions are only part of compliance. Large employers also face reporting obligations that document who was offered coverage and what kind of coverage was made available. These reports are critical because they help the IRS determine whether the employer satisfied the ACA mandate.

The key forms are generally the employer transmittal and employee statements used to report offers of coverage. Employers that fail to file correctly, or that file incomplete information, may increase their exposure even if the underlying health plan is otherwise compliant.

- Annual reporting: Large employers must report coverage information to the IRS.

- Employee statements: Workers may receive proof of the coverage offer they were given.

- Accuracy matters: Missing or incorrect data can lead to compliance problems.

What Employers Should Review Internally

Employers trying to stay compliant should treat ACA review as an ongoing process, not a once-a-year task. A good compliance review usually begins with workforce classification, then moves to plan design, contribution levels, and notice obligations. Employers should also examine whether benefit practices match the hours-tracking method they use for variable employees.

A practical review can include the following questions:

- Do we have 50 or more full-time employees, counting full-time equivalents?

- Are we measuring hours consistently for variable-hour workers?

- Does our plan provide minimum value and minimum essential coverage?

- Is the employee contribution affordable under ACA standards?

- Are dependent coverage rules and age limits correctly applied?

- Are reporting forms completed accurately and on time?

Common Mistakes That Create ACA Risk

Many ACA issues arise not from intentional noncompliance, but from administrative gaps. Employers sometimes misclassify workers, fail to track hours correctly, or assume that part-time staff do not need to be reviewed. Others rely on old plan language that no longer matches current federal requirements.

Another common mistake is focusing only on whether coverage exists, while ignoring whether it is affordable. A plan that is technically available but too costly to the employee may still fail the law. Likewise, employers may overlook reporting obligations until filing season, when records are incomplete or inconsistent.

| Common Error | Why It Matters |

|---|---|

| Miscounting hours | Can lead to wrong full-time determinations |

| Ignoring affordability | A plan may still trigger penalties if employee costs are too high |

| Incomplete reporting | Creates IRS exposure even when coverage was offered |

| Outdated plan documents | May conflict with current ACA rules |

FAQs

What counts as a full-time employee under the ACA?

In general, a full-time employee is someone who works at least 30 hours per week or 130 hours per month on average. Employers may use measurement methods to determine this for workers with variable schedules.

Do employers have to offer coverage to dependents?

For employers subject to the mandate, coverage generally must be offered to full-time employees and their dependent children. The ACA’s dependent rule usually extends coverage until a child reaches age 26.

What happens if coverage is offered but is too expensive?

If the employee share of the premium is not affordable under the ACA test, the employer may still face penalty exposure if the employee obtains subsidized marketplace coverage.

Are small employers required to follow the mandate?

Most employers below the 50 full-time employee threshold are not subject to the employer shared responsibility rules, though they may still offer coverage voluntarily and may have other compliance concerns.

Why is reporting so important?

Reporting shows the IRS which employees were offered coverage and whether the employer met ACA standards. Even a strong health plan can create problems if the reporting is late, incomplete, or inaccurate.

Practical Takeaways for Employers and Workers

For employers, the ACA is best understood as a combination of coverage, cost, eligibility, and paperwork rules. A compliant plan must be offered to the right employees, priced within the affordability limit, and documented properly. For workers, the law provides a stronger baseline of access to employer-sponsored health coverage, especially for those who work full time or whose schedules move over time.

Employers that use clear measurement systems, keep plan documents current, and monitor affordability are better positioned to avoid penalties and reduce employee confusion. Workers, meanwhile, benefit from knowing that coverage eligibility may depend on more than job title or weekly schedule; hours worked, plan design, and reporting all play a role.

References

- Affordable Care Act – SOU Human Resources — Southern Oregon University Human Resources. 2025. https://hrs.sou.edu/benefits-and-leaves/health-benefits/affordable-care-act/

- Complying with the Affordable Care Act — Government Finance Officers Association. 2024. https://www.gfoa.org/materials/complying-with-the-affordable-care-act

- Affordable Care Act tax provisions for employers — Internal Revenue Service. 2025. https://www.irs.gov/affordable-care-act/employers

- Affordable Care Act – U.S. Department of Labor — U.S. Department of Labor, Employee Benefits Security Administration. 2025. https://www.dol.gov/agencies/ebsa/laws-and-regulations/laws/affordable-care-act/for-employers-and-advisers

- Affordable Care Act | 1095-C — Benefit Options, State of Arizona. 2025. https://benefitoptions.az.gov/aca

Similar Articles

Read full bio of Sneha Tete