Legal Issues with Bank Deposits

Understand the most common problems with bank deposits, your legal rights as a depositor, and how to protect your money when things go wrong.

Bank deposits are at the core of modern personal and business finance. When you put money into a bank account, you expect the funds to be accurately recorded, safely stored, and available when needed. Yet errors, delays, and disputes involving deposits are more common than many customers realize, and they can raise important legal questions about who bears the loss and how problems should be resolved.

This article explains how bank deposits work from a legal perspective, highlights typical problems that arise, and outlines the rights and responsibilities of both banks and customers. It also offers practical guidance for responding to deposit disputes and minimizing risk in everyday banking.

Understanding the Legal Nature of a Bank Deposit

To understand deposit problems, it helps to know what legally happens when you place money in a bank. In most jurisdictions, a bank deposit is not a simple safekeeping arrangement; instead, it creates a debtor–creditor relationship between you and the bank.

- Ownership transfer: Once you deposit funds, the bank typically becomes the owner of the money. You receive a claim against the bank for the amount shown in your account.

- Bank as debtor: The bank owes you the balance recorded in your account and must honor withdrawals and payment instructions according to the agreed terms.

- Contractual relationship: Your rights are defined by the account agreement, applicable banking laws, and regulations governing consumer financial products.

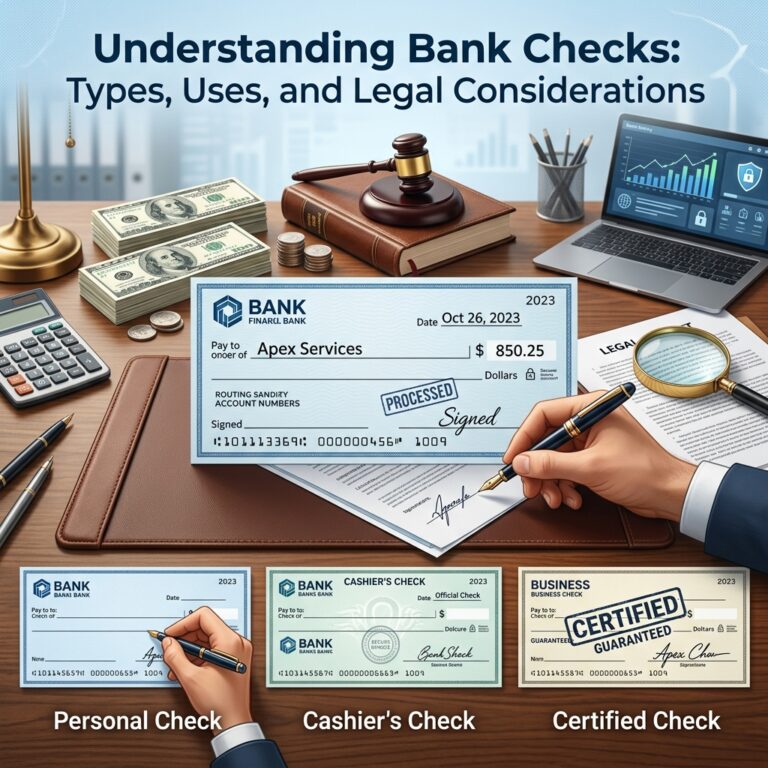

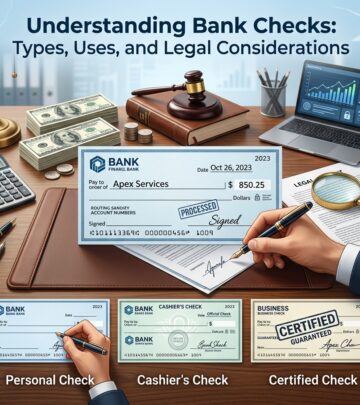

Understanding Bank Checks: Types, Uses, and Legal Considerations >

Because of this legal structure, disputes about deposits are usually treated as questions of contract, negligence, and regulatory compliance, rather than simple property disputes.

Common Problems Involving Bank Deposits

Deposit-related issues can arise at different stages of the transaction: when the deposit is initiated, while it is being processed, or after the funds have been credited to the account. Some of the most frequent problems include:

- Missing or uncredited deposits: A deposit made at a branch, ATM, or via mobile app does not appear in the account.

- Incorrect deposit amounts: The bank records a different amount than what was actually deposited.

- Delayed availability of funds: Deposited money is subject to holds or extended processing times.

- Duplicate or erroneous credits: The account shows more money than was actually deposited, often due to a system error.

- Fraudulent deposits or counterfeit checks: Deposits involving fake checks or unauthorized activity result in reversals and potential overdrafts.

Each type of problem raises distinct legal and practical questions about evidence, responsibility, and remedies.

Illustrative Comparison of Deposit Issues

| Type of Problem | Typical Cause | Key Legal Question |

|---|---|---|

| Missing deposit | Clerical error, system failure, ATM malfunction | Can the customer prove the deposit was made, and did the bank exercise reasonable care? |

| Incorrect amount | Data entry error, misread check, damaged cash | Whose records control, and is the bank obliged to correct the error promptly? |

| Delayed availability | Regulatory hold periods, risk controls, compliance checks | Is the hold permissible and properly disclosed under governing law? |

| Erroneous extra funds | Software glitch, misapplied deposit | Is the customer allowed to keep the extra money, or must it be returned? |

| Fraudulent deposit | Counterfeit check or unauthorized transaction | Who bears the loss when deposited funds are later reversed? |

Bank Duties in Handling Deposits

Banks are subject to legal and regulatory obligations designed to ensure that deposits are processed fairly and securely. In many countries, consumer protection rules require clear disclosures and prompt corrections of errors.

- Duty of care: Banks must use reasonable care in receiving, recording, and posting deposits, including maintaining secure and reliable systems.

- Error resolution procedures: Consumer regulations often mandate investigation and correction of certain account errors within specified time frames when timely notice is provided by the customer.

- Funds availability rules: In the United States, for example, Regulation CC sets maximum time limits for making funds from certain deposits available and requires notice of longer holds.

- Recordkeeping requirements: Financial institutions must retain transaction records, which are crucial when reconstructing what occurred in a disputed deposit.

Failure to meet these obligations may expose a bank to regulatory action or civil liability, particularly where customers suffer financial harm because of mishandled deposits.

Customer Responsibilities and Risk Management

Customers also have responsibilities in the deposit process. Courts and regulators often consider whether a depositor acted reasonably in monitoring accounts and retaining documentation.

- Maintain evidence: Keep deposit receipts, ATM slips, mobile confirmation numbers, and copies of checks.

- Review statements promptly: Regularly check account activity and monthly statements and report discrepancies quickly.

- Follow account terms: Comply with any notice deadlines or dispute procedures specified in the account agreement.

- Avoid risky practices: Do not rely on unverified funds from unknown or suspicious sources, especially in the case of large check deposits.

When a dispute arises, a depositor who can demonstrate diligence and provide documentation is usually in a stronger position to seek correction or reimbursement.

How Deposit Problems Typically Arise

Deposit problems often originate in one of three areas: human error, system malfunction, or fraudulent activity. Understanding these sources can clarify how responsibility may be allocated.

Human Errors

Manual processing is still involved in many deposits, particularly for cash and checks handled at branches. Errors can include miscounted cash, misread check amounts, or misapplied account numbers. When bank employees make mistakes, the institution is generally responsible for correcting them, provided the depositor gives adequate notice and evidence.

Technical and System Failures

Electronic deposits—such as payroll direct deposits and mobile check deposits—depend on complex payment systems. Network outages or processing glitches can delay or disrupt funds posting across multiple banks. In such cases, customers may experience delays rather than permanent loss, but the impact can be serious if they rely on the funds for time-sensitive obligations.

Fraud and Unauthorized Activity

Fraudulent deposits can be especially complicated. For example, a customer may deposit a check that looks legitimate, spend the funds once they appear available, and later discover that the check was counterfeit. When the check is returned unpaid, the bank may reverse the deposit and assess fees, leaving the account overdrawn. Laws and regulations typically place the risk of counterfeit checks on the depositor, unless the bank fails to exercise reasonable care in processing or has given specific assurances.

Legal Consequences of Erroneous Deposits

Not every deposit error results in litigation, but serious or unresolved problems can lead to legal claims. Key issues include liability for missing funds and obligations to return money posted by mistake.

Liability for Missing or Incorrect Deposits

When a deposit is not credited or is credited incorrectly, courts often look at three factors:

- Proof of deposit: Receipts, video records from ATMs, and bank logs help show whether a deposit was actually made.

- Timely notice: Many account agreements require customers to report errors within a certain number of days after receiving a statement.

- Bank’s investigation: Financial institutions are expected to conduct a reasonable investigation and correct confirmed errors.

If a bank fails to perform a reasonable investigation or ignores clear evidence, the customer may pursue claims such as breach of contract, negligence, or violations of consumer protection statutes.

Obligation to Return Funds Credited by Mistake

Customers sometimes discover unexpectedly high balances because of an erroneous credit. Although it may be tempting to treat the extra money as a windfall, the law in many jurisdictions requires customers to return funds that were deposited in error. Spending money that you know or should know was mistakenly credited can lead to legal liability, including claims for unjust enrichment and, in extreme cases, criminal charges if there is deliberate misuse.

Deposit Insurance and Bank Failure

Deposit insurance schemes are designed to protect depositors if the bank itself fails, rather than to resolve routine transaction errors. They play an important role in reassuring customers that their deposits will be protected up to certain limits if a bank becomes insolvent.

- Coverage limits: In the United States, the Federal Deposit Insurance Corporation (FDIC) generally insures deposits up to a standard amount per depositor, per insured bank, per ownership category.

- Eligible accounts: Coverage typically applies to standard deposit products such as checking accounts, savings accounts, and certificates of deposit, provided the institution is insured.

- Separate categories: Different ownership categories (for example, individual accounts versus joint accounts) may each receive separate coverage, allowing some customers to be protected beyond the basic limit when requirements are met.

Deposit insurance does not directly cure individual deposit errors, but it ensures that properly recorded deposits are protected if the bank collapses. Customers should verify that their bank is covered by the relevant deposit insurance system and understand which account types are eligible.

Practical Steps When a Bank Deposit Problem Occurs

When you suspect an error or problem with a deposit, prompt and organized action is essential. The following steps help preserve your rights and increase the chances of a quick resolution:

- Gather documentation: Collect all evidence related to the deposit, including receipts, screenshots, check copies, and any communication with the bank.

- Contact the bank immediately: Report the issue using the bank’s official channels—branch representatives, phone support, or secure messaging—and note the date, time, and names of employees you speak with.

- Submit a written complaint: If the problem is not resolved quickly, put your complaint in writing and request a formal investigation and response.

- Monitor account activity: Continue to watch your account for changes, holds, or reversals related to the disputed deposit.

- Escalate to regulators if needed: If you believe the bank is not following applicable rules, you may be able to file a complaint with a financial regulator or consumer protection agency.

- Consult legal counsel: For complex or high-value disputes, especially where significant losses are involved, seek advice from an attorney experienced in banking or consumer law.

Preventive Measures for Safer Deposits

While not all errors can be avoided, careful habits and awareness of legal rules can reduce the risk of serious deposit problems.

- Use reputable institutions: Choose banks with strong regulatory oversight and track records of reliable customer service.

- Verify account information: Double-check account numbers and names when depositing via transfer, mobile app, or third-party services.

- Keep records for a reasonable period: Store deposit-related documentation in a secure place until you have verified that funds were correctly posted and your statements are accurate.

- Enable alerts: Many banks offer real-time notifications for deposits and withdrawals, which can help you detect errors quickly.

- Be cautious with checks from unknown parties: Wait for full clearing of funds and be skeptical of transactions that involve forwarding or returning money related to a deposit, as these are often associated with scams.

FAQs About Bank Deposit Problems

1. If my deposit does not appear, how long should I wait before contacting the bank?

You should contact the bank as soon as you notice that a deposit appears to be missing or delayed, especially if the funds are needed for immediate obligations. Some deposits, such as checks, may legitimately take a day or more to post, but reporting a potential problem early helps trigger an investigation and protects your rights.

2. Can the bank place a hold on my deposit even if I have an urgent need for the money?

Banks may place holds based on regulatory rules, risk assessments, and internal policies, particularly for large or unusual deposits. Although you may explain your need for the funds, the bank is generally allowed to follow lawful hold policies as long as they are properly disclosed and comply with applicable regulations.

3. What happens if a deposited check turns out to be fraudulent?

If a check you deposited is later identified as fraudulent or counterfeit, the bank may reverse the deposit and charge fees, potentially causing an overdraft. In many cases, the customer bears the risk of depositing a counterfeit item, especially if the bank processed it using standard care. Consumer regulations may limit or clarify liability in certain circumstances, but they do not guarantee protection from all losses related to fraudulent deposits.

4. Am I allowed to keep extra money that appears in my account because of a bank error?

Generally, you are not entitled to keep funds that were credited to your account by mistake. Using money you know or should know is not yours can lead to legal claims and, in serious cases, allegations of misuse or fraud. You should notify the bank and allow it to correct the error.

5. Does deposit insurance help if the bank mishandles a single deposit?

Deposit insurance is primarily designed to protect customers if an insured bank fails, not to resolve individual transaction errors. Mishandled deposits are usually addressed through the bank’s error resolution processes and consumer protection regulations. However, once a deposit has been correctly recorded in an insured account, deposit insurance may protect it against loss from bank insolvency up to applicable limits.

References

- Accounts: common problems — Consumer Financial Protection Bureau. 2023-05-15. https://www.consumerfinance.gov/es/herramientas-del-consumidor/cuentas-bancarias/respuestas/problemas-comunes/

- FDIC Deposit Insurance at a Glance — Federal Deposit Insurance Corporation. 2022-11-01. https://www.fdic.gov/resources/deposit-insurance/

- What happens to your money if the bank where you keep it collapses? — Univision. 2023-03-13. https://www.univision.com/noticias/dinero/que-pasa-con-tu-dinero-si-el-banco-donde-lo-guardas-colapsa-signature-bank-y-silicon-valley-bank

- Qué pasa con los depósitos bancarios — Banco Internacional (COSEDE information). 2022-09-01. https://www.bancointernacional.com.ec/educacion-financiera/que-pasa-con-los-depositos-bancarios/

- Las 7 reclamaciones bancarias más comunes — Duriva. 2024-01-10. https://duriva.com/las-7-reclamaciones-bancarias-mas-comunes/

- Bancos reportan problemas con sistema de depósitos directos — WFLA / Tampa Hoy. 2024-03-08. https://www.wfla.com/tampa-hoy/nacional/bancos-reportan-problemas-con-sistema-de-depositos-directos/

Similar Articles

Read full bio of medha deb