Estate Planning Strategies for Property Owners

Learn how to protect real estate, reduce complications, and transfer property smoothly to your chosen heirs with a solid estate plan.

Owning real estate is often one of the largest financial and emotional investments a person makes. Yet many property owners overlook the importance of a tailored estate plan until it is too late. An effective plan not only determines who receives your property but also how and when they receive it, what taxes may be owed, and whether probate or family conflict will complicate the transfer.

This guide explains key estate planning tools and strategies for property owners, including wills, trusts, deeds, beneficiary designations, and lifetime transfers. It is designed to help you think through practical decisions, reduce uncertainty for your heirs, and work more effectively with legal and financial professionals.

Why Estate Planning Matters Especially for Real Estate

Estate planning is the process of deciding how your assets and personal wishes will be managed and distributed if you become incapacitated or after you die. Real estate introduces unique issues that make planning particularly important:

- High value and illiquidity — Property is often expensive and cannot be easily divided or sold quickly.

- Shared use and emotional attachment — Homes and family vacation properties carry sentimental value and may be used by multiple family members.

- Title and ownership complications — How a property is titled (sole ownership, joint tenancy, etc.) directly affects who inherits it and whether probate is required.

- Tax consequences — Transfers may trigger estate, gift, or capital gains taxes and influence the overall value of your estate.[10]

Key Legal Documents Every Family Should Have >

An estate plan brings structure to these issues, setting clear instructions for transfer and ongoing management and helping your beneficiaries avoid unnecessary costs and delays.

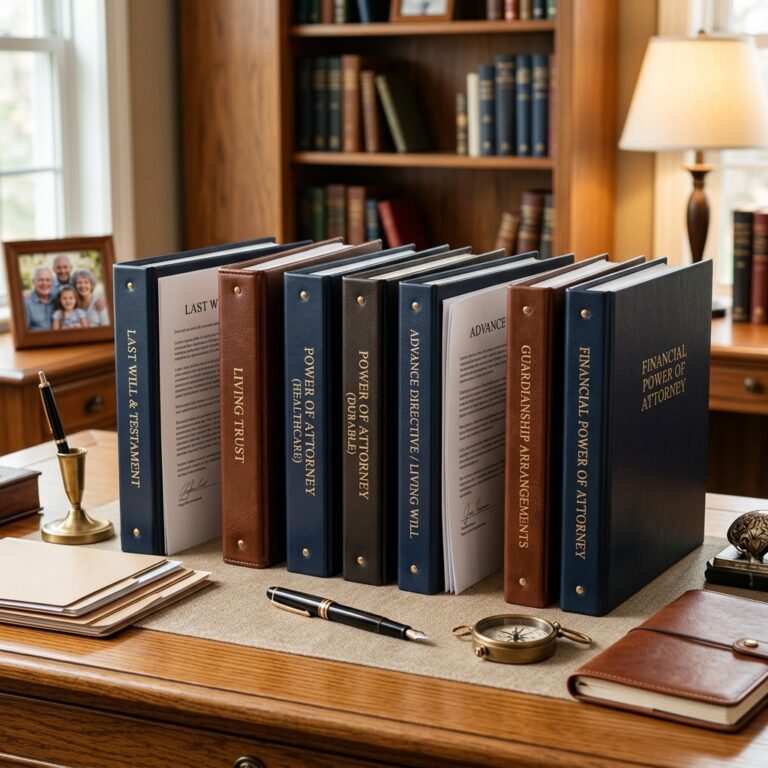

Core Estate Planning Documents Every Property Owner Should Consider

While each estate plan is unique, several core documents are commonly recommended, particularly for those who own real estate:

- Last will and testament — Directs who receives your property and appoints an executor to manage your estate.

- Revocable living trust — Holds property during your lifetime and provides instructions for management and distribution, often avoiding probate.

- Financial power of attorney — Authorizes a trusted person to handle financial decisions, including property management, if you are incapacitated.

- Health care documents — Advance directives and health care powers of attorney guide medical decision-making; while not property-focused, they support a comprehensive plan.

These documents interact with how your property is titled and with any special deeds or beneficiary designations you use. Reviewing these together allows you to build a coordinated plan rather than relying on a single tool.

How Property Ownership Affects Your Estate Plan

The way real estate is titled today often determines who will own it tomorrow, sometimes regardless of what your will says. Common ownership structures include:

| Ownership Type | Key Features | Estate Planning Impact |

|---|---|---|

| Sole ownership | One person holds title. | Property typically passes through probate under the will or state law. |

| Joint tenancy with right of survivorship | Two or more owners; survivor automatically receives the property. | Avoids probate for that property; may override will instructions. |

| Tenancy in common | Each owner holds a share that can be transferred separately. | Each share passes according to that owner’s will or intestacy laws. |

| Title in a living trust or entity (e.g., LLC) | Trust or entity holds legal title; individuals hold beneficial interests. | Transfer rules follow the trust or governing documents; can streamline succession. |

Before drafting new documents, review all current deeds, mortgages, and ownership agreements. Aligning title with your estate plan helps avoid conflicting instructions and unintentional transfers.

Options for Passing Your Home or Other Real Estate to Heirs

There is no single best method to transfer property; the right approach depends on your goals, family situation, and tax considerations. Common options include co-ownership, wills, trusts, beneficiary deeds, and lifetime gifts or sales.

Passing Property Through a Will

A will is often the cornerstone of an estate plan and can specify who receives your home or other real estate after death. Advantages include:

- Flexible instructions about who inherits property, including individuals or charities.

- Coordination with other assets, debts, and personal wishes.

- Ability to appoint guardians for minor children and an executor to oversee the estate.

However, property transferred by will typically passes through probate, which can be time-consuming and may involve court fees. For some owners, combining a will with other tools like trusts or beneficiary deeds can reduce probate exposure while still ensuring clear instructions.

Using a Revocable Living Trust for Real Estate

A revocable living trust is a widely used tool for property owners who want more control and privacy.

- You transfer your property into the trust, often by retitling the deed in the trust’s name.

- You usually act as both the grantor and trustee during your lifetime, keeping control of the property.

- At your death, a successor trustee follows the trust instructions to distribute or manage the property, typically without probate.

Benefits for property owners include:

- Probate avoidance in many situations, including when property is located in multiple states.

- Continuity of management if you become incapacitated.

- Privacy, since trust administration is usually not a public court proceeding.

Trusts require initial setup and funding, and professional advice is strongly recommended. They can also be combined with entities such as limited liability companies (LLCs) for additional liability or tax planning.

Co-Ownership and Joint Tenancy

Some property owners consider adding children or other heirs as co-owners to simplify transfer. While joint tenancy can allow property to pass automatically to a surviving joint owner, there are important trade-offs:

- Co-owners typically gain immediate rights, including the ability to sell or mortgage their interest.

- Lifetime gifts of property may limit tax benefits such as a step-up in basis at death, potentially increasing capital gains tax if the property is later sold.

- Creditors of a co-owner may have claims against the property.

Co-ownership can be useful in some circumstances, but it should be evaluated carefully with financial and legal professionals rather than used as a quick fix.

Beneficiary Deeds and Transfer-on-Death Designations

In certain states, property owners can sign a transfer-on-death (TOD) or similar beneficiary deed that names who should receive the property when they die.

- The property passes directly to the named beneficiary outside probate.

- The owner retains control during life and can revoke or change the designation.

- Heirs may still benefit from a step-up in basis for tax purposes, depending on applicable law.

Because these deeds are state-specific, it is crucial to consult local law or a qualified attorney to confirm availability, formal requirements, and interaction with your broader estate plan.

Lifetime Gifts and Qualified Personal Residence Trusts

Some property owners prefer to transfer real estate during their lifetime. Approaches range from simple gifts to more advanced structures such as qualified personal residence trusts (QPRTs).

- Outright lifetime gifts can remove property from your estate but may have gift tax and capital gains implications.

- QPRTs allow you to transfer a primary or vacation residence to a trust at a reduced gift tax value while retaining the right to live in the home for a set term.

These strategies are best considered as part of comprehensive tax and estate planning, usually with guidance from a professional familiar with current tax laws.[10]

Planning for Ongoing Management, Costs, and Family Use

Estate planning for real estate involves more than deciding who receives ownership. Many families need clear guidance on how the property will be maintained, used, and potentially sold after the owner’s death.

Important questions include:

- Who will be responsible for property taxes, insurance, and maintenance?

- Should beneficiaries contribute equally to ongoing expenses, or will one person take the lead?

- Will the property be maintained as a family asset for shared use, or sold to distribute cash?

- Are there plans for major improvements or renovations, and how will these be financed?

Owners can document expectations directly in a will, trust, or a separate shared-use agreement. When an LLC or trust holds the property, governing documents can address scheduling, buyout rights, and dispute resolution among beneficiaries.

Tax Considerations for Property in an Estate Plan

Tax laws change regularly, and the impact on real estate can be significant. While specific advice requires professional analysis, property owners should be aware of several general concepts:[10]

- Estate and gift taxes — Large estates may trigger federal or state estate tax; some strategies focus on keeping the taxable estate below threshold levels.[10]

- Income and capital gains taxes — When heirs sell inherited property, capital gains are often calculated using a stepped-up basis equal to the fair market value at the decedent’s death.

- Property tax rules — Ownership transfers can affect local property tax assessments or exemptions.

In many cases, the overriding financial goal is to maximize the amount preserved for beneficiaries while still meeting family needs and personal objectives.[10] Coordinating your estate plan with tax, insurance, and retirement planning helps address both immediate and long-term implications.

Building and Updating Your Estate Plan as a Property Owner

Estate planning is not a one-time event. Laws, property values, and family circumstances evolve, making periodic review essential.

Practical steps include:

- Clarify your goals for each property (e.g., keep in family, sell, donate).

- Make a complete inventory of your real estate and related debts.

- Gather deeds, mortgage documents, insurance policies, and tax records.

- Consult with an attorney and other advisors about appropriate tools such as wills, trusts, and beneficiary deeds.

- Review and update documents every few years or after major life events such as marriage, divorce, birth of a child, or relocation.

- Discuss your plans with affected family members to reduce uncertainty and conflict.

By taking these steps, property owners can help ensure their wishes are honored and that heirs are prepared for both the financial and practical responsibilities of ownership.

Frequently Asked Questions About Estate Planning for Property Owners

Does my property automatically follow my will?

Not always. Property titled in joint tenancy with right of survivorship, held in a trust, or subject to a transfer-on-death deed may bypass your will and pass directly to the designated person. This is why reviewing title documents is as important as drafting the will itself.

Is a trust always better than a will for real estate?

Neither tool is universally better; each serves different purposes. A will is simpler to create and still essential even when you have a trust, while a revocable living trust can help avoid probate, provide continuity of management, and add privacy. Many property owners use both.

Can I just add my child to the deed to avoid probate?

Adding a child as a co-owner may avoid probate for that property but can introduce tax implications, creditor risks, and loss of independent control. Professionals often recommend evaluating alternatives such as beneficiary deeds or trusts before changing title.

How often should I review my estate plan if I own real estate?

Experts commonly recommend reviewing estate planning documents every three to five years or whenever major changes occur, such as acquiring or selling property, moving to another state, or experiencing significant family events.

Do I need a lawyer, or can I plan my estate on my own?

Basic steps, such as organizing documents and listing assets, can be done independently. However, because real estate involves complex issues of title, taxes, and state law, owner-focused estate planning typically benefits from professional counsel. An attorney familiar with property and estate planning can help you select appropriate tools and ensure they work together correctly.

References

- Estate Planning Information & FAQs — American Bar Association. 2024-03-01. https://www.americanbar.org/groups/real_property_trust_estate/resources/estate-planning/

- What Is Estate Planning? Key Steps to Protect Your Family and Finances — National Council on Aging. 2023-08-10. https://www.ncoa.org/article/what-is-estate-planning-key-steps-to-protect-your-family-and-finances/

- Ways to Leave Your House to a Loved One — Fidelity Investments Learning Center. 2022-11-15. https://www.fidelity.com/learning-center/personal-finance/estate-planning

- Estate Planning for Family Real Estate — Commerce Trust Company. 2023-05-05. https://www.commercetrustcompany.com/research-and-insights/articles/estate-planning-for-family-real-estate

- Planning for the Future — U.S. Department of the Interior, Office of the Special Trustee. 2025-01-01. https://www.doi.gov/ost/planning-future

- What Is Estate Planning? — EstatePlanning.com. 2023-06-01. https://www.estateplanning.com/what-is-estate-planning

- Basic Estate Planning: Introduction — Ohio State University Extension (Ohioline). 2012-01-01. https://ohioline.osu.edu/factsheet/ep-1

Similar Articles

Read full bio of medha deb