Protecting Non‑Spouse Joint Bank Accounts From Levies

Understand how creditors reach non‑spouse joint bank accounts, what “traceable contributions” and exempt funds mean, and how to defend your money.

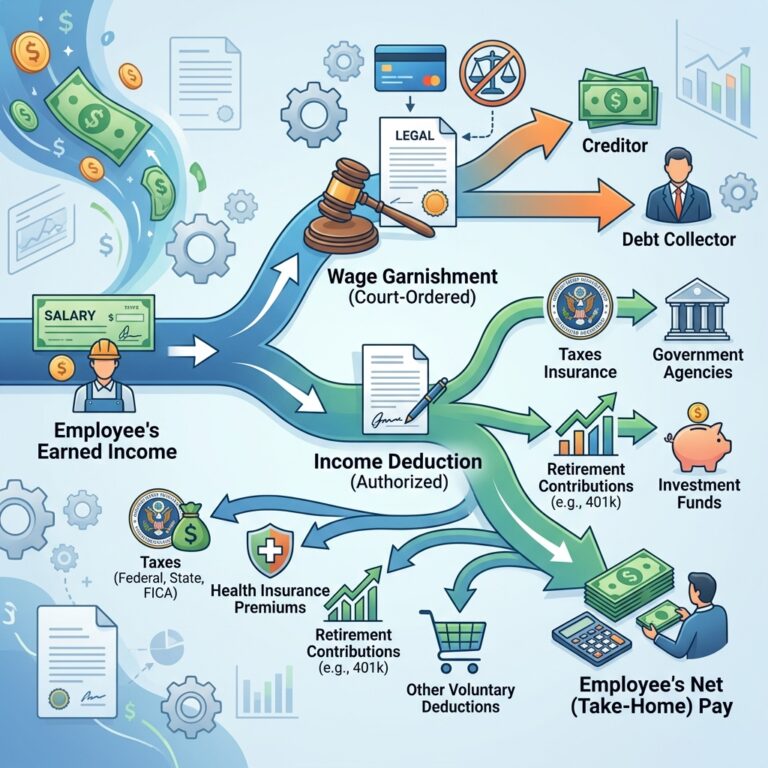

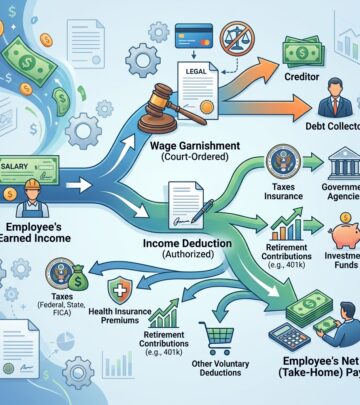

Joint bank accounts are often opened for convenience, family support, or shared financial goals. But when one co‑owner owes a debt, a joint account can unexpectedly become a target for creditor bank levies, even if the other co‑owner has never missed a payment or signed a contract with that creditor. Bank account levies (also called garnishments) allow a creditor, armed with a court judgment, to freeze and remove money from an account, including an account held jointly with a non‑spouse.

This guide explains how levies on non‑spouse joint bank accounts work, how ownership of funds is determined, which deposits are protected by law, and what steps a non‑debtor can take to defend their money. It is general information, not legal advice; laws vary by state, so consulting a qualified attorney is essential.

1. What Is a Bank Levy and When Can It Hit a Joint Account?

A bank levy is a legal process that allows a judgment creditor to take money directly from a debtor’s bank account to satisfy an unpaid court judgment. Before a levy can occur, several steps typically happen:

- The creditor sues the debtor in civil court for the unpaid debt.

- The creditor wins and obtains a judgment that legally confirms the debt.

- The creditor secures a court order or writ of execution authorizing a bank levy.

- The sheriff or other enforcement officer serves legal papers on the bank.

Once served, the bank usually must freeze the funds in the account up to the amount indicated in the writ and then hold those funds until the court orders turnover or releases the levy. During this period, account holders may lose access to their money, even if the funds ultimately turn out to be legally protected or belong to a non‑debtor co‑owner.

Online Consumer Data Collection Laws >

1.1 Non‑Spouse Joint Accounts: Why Creditors Can Reach Them

Creditors generally may levy a bank account that bears the debtor’s name, including a joint account with a non‑spouse co‑owner. In many jurisdictions, a joint account is viewed as a single pool of funds to which each co‑owner has full withdrawal rights, making it an accessible asset for creditor enforcement.

Key implications for non‑spouse joint accounts:

- Non‑debtors are exposed: The co‑owner who does not owe the debt can still have their money frozen and, potentially, taken unless they contest the levy and prove their ownership.

- Presumptions of ownership: Courts often start with a presumption that funds in a joint account belong to the co‑owners in equal shares, unless evidence shows otherwise.

- State‑specific rules: Some states allow creditors to take all funds in a joint account; others limit access to the debtor’s share or require additional court proceedings.

Because these rules differ by state, the rights of a non‑spouse joint account holder can vary dramatically depending on where the account is located and which law applies.

2. Who Owns the Money? Understanding Legal Ownership in Joint Accounts

Ownership in a joint account is not always as simple as “we each own half.” In practice, courts look to both statutory rules and evidence of contributions to determine how much of the money belongs to the debtor versus the non‑debtor co‑owner.

2.1 Common Legal Approaches to Ownership

| Approach | Core Rule | Effect on Levies |

|---|---|---|

| Equal shares presumption | Each joint owner is presumed to own 50% (or equal fractions) of funds. | Creditor may initially reach the debtor’s presumed share, unless evidence shows different actual contributions. |

| Net contributions rule | Each party owns funds in proportion to their net deposits into the account. | Non‑debtor can protect funds by proving they made most or all contributions; creditor limited to debtor’s contribution share. |

| Full access jurisdictions | In some states, creditors may reach all funds in certain joint accounts unless co‑owners successfully contest. | Non‑debtor may need to file objections quickly to reclaim funds based on contribution evidence and exemptions. |

For example, Virginia law states that a joint account belongs to the parties in proportion to the net contributions by each during their lifetimes. Other states apply a default 50/50 ownership presumption, which can be rebutted with evidence.

2.2 Traceable Contributions: The Non‑Debtor’s Primary Defense

The concept of traceable contributions is crucial for non‑debtors. It refers to the ability to show, through documentation, that deposits to the joint account came from the non‑debtor and not the debtor. If a court accepts that certain funds are traceable to the non‑debtor, those amounts are generally not available to satisfy the debtor’s judgment.

Typical documents used to trace contributions include:

- Pay stubs and employer direct deposit records

- Government pension or retirement statements

- Insurance or annuity payment records

- Bank and credit union statements showing transfers from other accounts

- Benefit award letters and deposit histories for public benefits

The stronger and more continuous the documentation, the easier it is for a non‑debtor to persuade the court that specific funds should be excluded from the levy and returned.

2.3 Convenience Accounts and the Reality of Ownership

Some joint accounts are opened primarily so that one person can help another manage finances—for example, an adult child added to an elderly parent’s account to assist with bill payments. In these scenarios, courts may treat the account as a “convenience account”, meaning the added person does not truly own the funds despite their name appearing on the account.

To show that a joint account is a convenience account, the non‑debtor generally must satisfy a reality of ownership test, such as:

- Demonstrating that one person (often the non‑debtor) supplied nearly all funds in the account.

- Showing that the debtor rarely, if ever, used the account for personal spending or deposits.

- Providing patterns of deposits and withdrawals that reflect one party’s exclusive financial use.

If the court concludes that the reality of ownership lies with the non‑debtor, it may shield the account from the debtor’s creditors or significantly limit what the creditor can take.

3. Exempt Funds: Deposits That Are Protected From Garnishment

Even when a creditor properly levies a joint account, not all money in the account is fair game. Both federal and state laws protect certain types of income from garnishment, and these protections often continue even after the money is deposited into a bank account.

3.1 Common Categories of Exempt Income

Although details vary by jurisdiction, the following types of funds are widely recognized as either fully or partially exempt from bank account garnishment:

- Social Security retirement and disability benefits

- Supplemental Security Income (SSI)

- Worker’s compensation payments

- Unemployment benefits

- Certain disability benefits

- Child support and, in some states, alimony or spousal support

- Some forms of public assistance and government benefits

- A protected portion of wages (often a percentage such as 25% or more, depending on law)

According to consumer guidance from United Way, these protected sources do not automatically lose their protection once deposited, but the account holder may need to affirmatively claim exemptions and provide proof of the funds’ origin.

3.2 Proving That Deposits Are Exempt

To keep exempt funds safe in a joint account, the non‑debtor or debtor must typically show that the deposits derive from a legally protected source and are therefore not available to general creditors.

Evidence used to establish exemptions can include:

- Benefit award letters from Social Security or other agencies

- Deposit records clearly labeling direct deposits as government benefits or support payments

- Payroll records or court orders reflecting child support or alimony payments

- Documentation linking each deposit to a specific exempt program

Because joint accounts pool funds, it can become challenging to distinguish exempt deposits from non‑exempt ones after months or years of transactions. Maintaining separate accounts for exempt income or meticulous records can significantly strengthen exemption claims.

4. What Happens During a Levy: Process and Immediate Impacts

Once a levy is served on the bank, the following sequence commonly occurs:

- Account freeze: The bank temporarily freezes some or all available funds up to the amount specified in the writ.

- Notice to account holders: The bank or enforcement officer sends notice of the levy, explaining rights and deadlines to challenge it.

- Evaluation of exemptions: The bank and sheriff may make an initial determination about obviously protected funds, such as Social Security deposits.

- Court involvement: The creditor requests a turnover order or similar court directive to have the frozen funds paid out.

During this period, checks may bounce, automatic payments can fail, and non‑debtors may be unable to access money they rely on for living expenses. Acting quickly is critical, especially when the non‑debtor believes that most or all of the funds do not belong to the debtor or are exempt.

4.1 Turnover Orders and Objections

In many states, a levy alone does not immediately transfer money to the creditor. A turnover order—a court order directing the bank to release funds—is required. At this stage, the non‑debtor often has one or two opportunities to contest:

- Opposing the creditor’s motion for turnover by filing written objections and presenting evidence of contributions and exemptions.

- Proactively filing a motion to vacate or modify the levy, arguing that the funds belong to the non‑debtor or are exempt.

Courts will then review ownership evidence, statutory exemptions, and state law presumptions before deciding how much, if any, of the frozen money should be delivered to the creditor.

5. Practical Strategies for Non‑Debtors to Protect Joint Account Funds

Non‑spouse joint account owners are not powerless when faced with a levy. Responsible planning and timely action can substantially reduce the risk that their funds will be taken.

5.1 Preventive Steps Before Any Levy Occurs

Even if no lawsuit is pending, consider these preventive measures:

- Maintain separate accounts for your own funds, especially exempt income, rather than relying solely on a joint account.

- Keep detailed records of all deposits, including pay stubs, benefit statements, and transfer confirmations.

- Monitor co‑owner debt risks—if the other account holder has serious unpaid debts, understand that your joint account may be targeted.

- Consider alternative arrangements, such as powers of attorney or convenience accounts clearly documented with the bank, instead of standard joint ownership.

5.2 Immediate Actions After Receiving a Levy Notice

If you receive notice that a joint account has been levied because of the other owner’s debt:

- Read the notice carefully to identify deadlines for objections and hearings.

- Gather documentation showing your deposits and any exempt sources of income.

- Consult a consumer or debt‑collection defense attorney to evaluate your options and prepare filings.

- Notify payees (landlord, utilities, lenders) if automatic payments or checks may bounce.

- Request a hearing or file objections within the required time frame, explaining why funds should be released.

Courts often strictly enforce deadlines. Missing them can result in permanent loss of funds, even when documentation suggests that the money belonged to the non‑debtor or was exempt.

5.3 Long‑Term Solutions for Debtors

For the debtor whose obligations triggered the levy, broader debt‑management strategies can reduce the risk of future disruptions:

- Negotiating payment plans or settlements with creditors before lawsuits escalate into judgments and levies.

- Seeking credit counseling to manage unsecured debts.

- Exploring bankruptcy when debts are overwhelming and other remedies have failed; bankruptcy can halt collection actions and may discharge some obligations.

While these strategies focus on the debtor, they indirectly protect non‑debtor co‑owners by reducing the likelihood that joint accounts will be targeted again.

6. Frequently Asked Questions About Non‑Spouse Joint Account Levies

6.1 Can a creditor take money from a joint account if I don’t owe the debt?

Yes. If your name is on a joint account with someone who owes a judgment, a creditor may levy the entire account or the debtor’s presumed share, depending on state law. You can contest the levy by proving that funds belong to you and not the debtor, or that they come from exempt sources.

6.2 Will the bank automatically protect Social Security or other benefits?

Banks and enforcement officers often review accounts for obvious exempt deposits, such as direct Social Security payments, and may initially protect some of those funds. However, you may still need to formally assert exemptions and provide documentation to ensure the money is fully protected.

6.3 What if my state presumes that joint account funds are owned equally?

In jurisdictions where joint accounts are presumed to be owned 50/50, creditors typically can reach the debtor’s presumed share first. That presumption can be overcome if you present strong evidence of your actual contributions showing that more—or all—of the funds are yours.

6.4 Can I close the joint account to avoid a levy once a lawsuit is filed?

Closing or moving funds after learning of a pending levy can be risky and may be viewed as an attempt to evade creditors, potentially leading to legal consequences. Courts and enforcement agencies may unwind transfers that appear fraudulent. Always seek legal advice before moving money in anticipation of collection actions.

6.5 Should I ever agree to a joint account with someone who has serious debt?

Using a joint account with someone who is heavily indebted increases the risk that your funds will be entangled in their creditors’ collection efforts. If shared access is necessary, alternatives like separate accounts, direct bill payments, or documented convenience arrangements may better protect you. Consulting a lawyer or financial advisor before opening a joint account in this situation is prudent.

References

- Can Creditors Garnish My Joint Account? — Nolo. 2023-05-10. https://www.nolo.com/legal-encyclopedia/bank-levies-joint-accounts-nonspouse.html

- Collect money from a bank account (bank levy) — Judicial Council of California. 2024-01-01. https://selfhelp.courts.ca.gov/civil-lawsuit/judgment/collect/bank-levy

- Non-Spouse Joint Bank Account Levy Lawyers — LegalMatch. 2022-11-15. https://www.legalmatch.com/law-library/article/non-spouse-joint-bank-account-levy-lawyers.html

- § 6.2-606. Ownership during lifetime; garnishment, attachment, or levy — Code of Virginia. 2020-07-01. https://law.lis.virginia.gov/vacode/title6.2/chapter6/section6.2-606/

- Joint Bank Account Turnover Proceedings in New York — The Langel Firm. 2023-05-18. https://www.thelangelfirm.com/debt-collection-defense-blog/2023/may/can-creditors-seize-your-joint-bank-account-know/

- Avoiding Account Garnishment — United Way Worldwide. 2021-09-30. https://www.unitedway.org/our-impact/financial-security/my-smart-money/avoiding-account-garnishment

- Ask a Financial Lawyer: Can Creditors Take Funds in a Joint Account? — Scura Law Firm. 2022-03-22. https://www.scura.com/blog/ask-a-financial-lawyer-can-creditors-take-funds-in-a-joint-account

Similar Articles

Read full bio of Sneha Tete